Most people are used to thinking about their wealth in purely financial terms. But consider the situation of someone who has just graduated from law school or medical school and is about to head into a high-paying job. Financial wealth for this person may be low–or even negative if there are student loans to be paid. But they do have an enormous non-financial asset, namely the skills and credential that will allow them to earn a high salary in the future.

Or compare two 21 year-olds, one with only a high school degree and one who has completed a college degree. Their financial wealth may be similar: again, if the college student has loans outstanding, the financial wealth of the college student may be lower. But on average, a college graduate has a nonfinancial asset that will allow them to earn a higher future salary.

Economists refer to this kind of nonfinancial personal asset as “human capital.” The idea behind the terminology is to he idea was to draw a parallel with physical capital. In each case, an economic actor incurs costs in the present that over time have a long-run payoff. With human capital, the costs can involve both money (say, college tuition) and also time (when you go beyond what’s strictly needed to do today’s job and acquire skills that will be applicable in the future). A broad view of human capital can include not just education and job experience, but also physical and mental health.

A team of researchers at McKinsey Global Institute have written a report focusing on one aspect of the topic: “Human capital at work: The value of experience (June 2, 2022). The McKinsey team looked at “a data set of de-identified job histories for approximately four million workers across the United States, Germany, the United Kingdom, and India.”

They find that for those early in a career, entry-level skills from the education system are a main determinant of wages. But over time, job experience is a bigger and bigger part of your human capital.

Here’s an illustration for the US workers in their data, over a 30-year working life. Salary rises over the lifetime. After 10 years, 61% of pay can be attributed to entry-level skills (from formal education), but after 30 years, 60% of pay can be attributed to work experience. Notice also that the pay raises over time are because of the rising role of work experience.

Of course, these results are an overall average. The report gives example of how the pay premium for higher experience (in a US context) is very large for some jobs like airline pilots and physicians, but not so large for jobs like maintenance and repair workers.

Not all job experience is created equal. People who switch to a different job with a different employer, in a way that stretches and expands their skills, will expand their experience-related human capital. This insight has implications both for workers and employers. For workers, the report offers these categories:

From our data set, we looked at a smaller universe of people with more than ten years of work history. Within it, four distinct archetypes emerge. They are not meant to convey individuals’ circumstances or motivation; they describe movement patterns and outcomes, with illustrative examples. — Experience seekers start with lower-than-average wages but propel themselves upward by moving roles more frequently than their peers and stretching their capabilities substantially each time. The cumulative effect gives them stronger wage growth than any other archetype. Consider someone who starts as an administrative assistant at one nonprofit before landing a job cultivating donors in the development department of another. From there, she joins a research hospital as a grant writer before stepping into a broader communications role. Eventually she becomes head of media relations for a major university. Our experience seeker has managed to cross over into new industries and functions. — Early movers make bigger leaps in the first part of their career. Someone may start in one field, quickly realize that their passion lies elsewhere, and then get a break that enables them to follow it. A graphic designer who makes print ads, for example, might become a user-experience designer early in her career. — Late movers stay put or make more incremental moves in the early stage of their career but eventually take a bolder step. Think of a seasoned journalist who goes into corporate communications, or a real estate agent who becomes a mortgage loan officer in a bank. This is by far the largest group in the sample. — Lock-ins change jobs less frequently, and when they do move, they do not make dramatic changes. This is not necessarily because someone is timid or stuck; they could also follow this strategy because they pursued what suited them from the start. Teachers, for example, have invested in specialized education and may have found their calling. However, lock-ins have the slowest wage growth, whether they start near the bottom or near the top. Doctors start at a very high salary but do not tend to make many role moves. While work experience accounts for 60 to 70 percent of lifetime earnings for experience seekers and early movers, that share is only about 30 percent for lock-ins.

There are implications for employers looking for talent, as well.

Most employers can benefit from challenging the status quo of how they select people for open roles. Instead of searching for “holy grail” external candidates whose prior experience precisely matches the responsibilities in an open role, leading organizations create systems for evaluating candidates based on their capacity to learn, their intrinsic capabilities, and their transferable skills. This requires designing assessments that are fit for purpose, focusing on the few core skills that matter for success in the role. It also involves removing biases that pigeonhole people into the roles they are already performing; this point is particularly important when it comes to existing employees. In our sample, more than half of all role moves undertaken by individuals involved a skill distance of more than 25 percent—and this implies that people often have latent capabilities that are not recognized by their current employers. If someone’s track record shows the acquisition of new skills over time, it probably means that person is capable of learning more. Employers should be less constrained about recruiting candidates from traditional sources and backgrounds, and more open to people who have taken unconventional career paths.

I write as someone who has had the same job title, with the same employer, for 36 years. In the categories given above, I’m a lock-in. I’ve been very happy with my job and what I do. But especially for those early in their careers, thinking in a serious way about whether your current employer is helping to develop the breadth and depth of your work experience human capital–or whether a job with an alternative employer might help you to do so–is likely to be at least as important to your lifetime financial well-being as the decisions you make about financial savings and investment.

The most recent OECD Economic Outlook report (June 2022) leads off with a discussion of how Russia’s attack on Ukraine is affecting the global economy. The first chapter begins like this (references to tables omitted):

The war in Ukraine has generated a major humanitarian crisis affecting millions of people. The associated economic shocks, and their impact on global commodity, trade and financial markets, will also have a material impact on economic outcomes and livelihoods. Prior to the outbreak of the war the outlook appeared broadly favourable over 2022-23, with growth and inflation returning to normality as the COVID-19 pandemic and supply-side constraints waned. The invasion of Ukraine, along with shutdowns in major cities and ports in China due to the zero-COVID policy, has generated a new set of adverse shocks. Global GDP growth is now projected to slow sharply this year to 3%, around 1½ percentage points weaker than projected in the December 2021 OECD Economic Outlook, and to remain at a similar subdued pace in 2023. In part, this reflects deep downturns in Russia and Ukraine, but growth is set to be considerably weaker than expected in most economies, especially in Europe, where an embargo on oil and coal imports from Russia is incorporated in the projections for 2023. Commodity prices have risen substantially, reflecting the importance of supply from Russia and Ukraine in many markets, adding to inflationary pressures and hitting real incomes and spending, particularly for the most vulnerable households. In many emerging-market economies the risks of food shortages are high given the reliance on agricultural exports from Russia and Ukraine. Supply-side pressures have also intensified as a result of the conflict, as well as the shutdowns in China. Consumer price inflation is projected to remain elevated, averaging around 5½ per cent in the major advanced economies in 2022, and 8½ per cent in the OECD as a whole, before receding in 2023 as supply-chain and commodity price pressures wane and the impact of tighter monetary conditions begins to be felt. Core inflation, though slowing, is nonetheless projected to remain at or above medium-term objectives in many major economies at the end of 2023.

The uncertainty around this outlook is high, and there are a number of prominent risks. The effects of the war in Ukraine may be even greater than assumed, for example because of an abrupt Europe-wide interruption of flows of gas from Russia, further increases in commodity prices, or stronger disruptions to global supply chains. Inflationary pressures could also prove stronger than expected, with risks that higher inflation expectations move away from central bank objectives and become reflected in faster wage growth amidst tight labour markets. Sharp increases in policy interest rates could also slow growth by more than projected. Financial markets have so far adjusted smoothly to tighter global financial conditions, but there are significant potential vulnerabilities from high debt levels and elevated asset prices.

While the report discusses a number of issues, two immediate concerns are commodity prices and refugees.

The major influence of Russia and Ukraine on the global economy is via their role as important suppliers in a number of commodity markets. Together they account for about 30% of global exports of wheat, 15% for corn, 20% for mineral fertilisers and natural gas, and 11% for oil. In addition, global supply chains are dependent on Russian and Ukrainian exports of metals (see below) and inert gases. The prices of many of these commodities increased sharply after the onset of the war, even in the immediate absence of any significant disruption to production or export volumes (Figure 1.1). … A particular concern is that a cessation of wheat exports from Russia and Ukraine could result in serious food shortages in many developing economies. There would be an acute risk not only of economic crises in some countries but also humanitarian disasters, with a sharp increase in poverty and hunger. The food supply shock could be compounded by fertiliser shortages and price rises, with Russia and Belarus major suppliers in many countries, putting agricultural output next year and perhaps beyond under stress.

On the magnitude of the refugees from Ukraine:

The war in Ukraine has generated a historic outflow of people fleeing the conflict, unseen in Europe since World War II. The Syrian conflict raged for two years before the number of refugees abroad reached three million in 2015-16, whilst this number was reached in less than 3 weeks for the war in Ukraine. By May 18, according to data from the UNHCR, more than 6.2 million people had fled Ukraine and an additional estimated 8 million were internally displaced. About 5.3 million Ukrainian refugees have reached the European Union. Close to 3.4 million Ukrainians crossed into Poland, almost 930 000 into Romania, 615 000 into Hungary and 427 000 into the Slovak Republic.

Over the medium-term, expect other consequences to arise: for example, from detaching European energy markets from Russian suppliers, from other shifts in global supply chains, and from costs of and reactions to international financial sanctions.

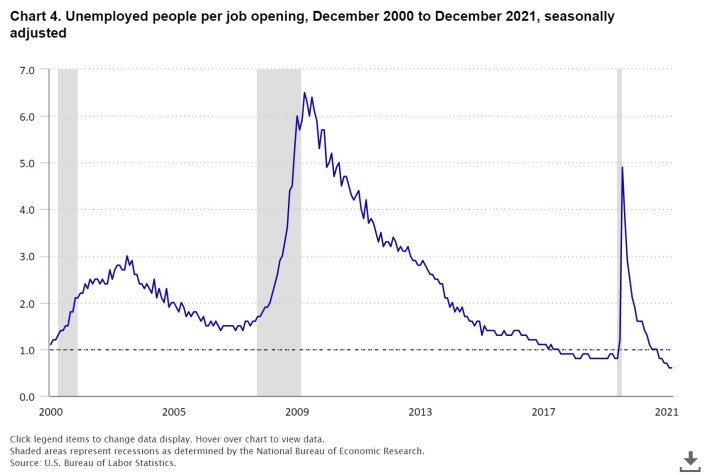

The dark blue line shows the number of unemployed people. The light blue line shows the number of job openings. The red line shows the gap between them. Notice that the red line is in negative territory: that is, the light blue line of job openings is higher than the dark blue line of unemployed people.

One can also look at these numbers as a ratio. This figure shows the ratio of unemployed people per job opening. You can see the rise immediately after each recession. The ratio is now below 1: again, the number of unemployed people is less than the number of job openings.

What’s striking to me is that this pattern of more job openings than unemployed is not just a post-pandemic phenomenon. It was part of a trend going back to the period after the Great Recession and up through early 2020, as well. Notice in the first figure that the number of job openings is steadily on the rise in the time before the pandemic–and recently as well–but the number of unemployed workers is falling. With all these job openings, why isn’t the unemployment rate even lower than 3.6%? Why do so many people seem to be finding it hard to get a job? Here are some of the (potentially overlapping) theories:

2) The Great Resignation theory suggests that there may be lots of jobs, but many of them don’t offer much in the way of pay, benefits, or career path. Thus, people who had those jobs in the past, or people who on the margin between working or not working, now have a greater tendency to opt out.

3) A pandemic hangover theory suggests that workers with health-related concerns may be especially slow to look for jobs. Similarly, after two years of disruption in school and child-care arrangements, a number of parents may be slow to look for jobs.

4) A transactions costs theory suggests that something about the nature of job search has changed. The old days of showing up at a store and filling out a job application in response to a help-wanted sign are, in many places, long-gone. Instead, firms post even entry-level jobs at their websites, and applying for a job can mean filling out pages of forms, uploading a resume, even an automated video interview. Firms have lots of reasons to have shifted their hiring in this way. But my sense is that the barriers of applying for a job in this way are real, perhaps especially for low-skilled workers. Workers must often plan to go through this application process at a number of potential employers, knowing that dozens or hundreds of other online applicants are doing the same thing. It may be that what a firm sees as a “job opening” is not the same as it used to be.

5) The US workforce is aging. The front edge of the post-World War II “Baby Boom” generation was born in 1945. That group hit age 65, and thus started retiring in force, around 2010. My sense is that a substantial number of older workers might be tempted to work, by the right mix of wages and job conditions, but don’t necessarily feel that they need to be pounding the internet (what we used to call “pounding the pavement”) looking for a job.

The underlying pattern here, at least up to the time before the pandemic recession, was a pair of countervailing trends in the labor force participation rate and the employment/population ratio. The falling labor force participation rate meant that a smaller share of adults were either employed or without a job but unemployed and looking for one. The rising employment/population ratio meant that out of the adult population, a larger share held jobs than before. Even before the pandemic recession, these patterns meant that firms were often seeking to hire people who didn’t count as officially unemployed, because they were out of the labor force and not actually looking for a job. This pattern of more job openings than unemployed existed before the pandemic. Except for periods of recession, it may be a new normal.

Why are Americans moving less over the past few decades?

I think there are at least two major developments behind that change. The first is that we’re just much more of a service economy and continue to become more and more services based. Say you’re a dentist. You don’t really think, “Well, I’ll move from Dallas to Denver, because Denver is where the teeth are.” Right? That wouldn’t make sense. In services, for the most part, you just pick where you want to live and you can stay there just fine. …

I think the other factor is that people are just better informed, partly because of the internet. They can figure out where they want to live earlier in life and then just stay there. Staying put comes with definite upsides. But it’s also the case when a downturn comes, maybe your labor markets don’t adjust the way they used to because everywhere is stuck in the same predicament. If everywhere looks a bit like Columbus, Ohio, or for that matter, Richmond, Virginia, there’s less moving.

Qualms about co-authorship and consensus in economics

I think macro has become underrated. One good thing about macro is that it’s not obsessed with co-authored papers. Co-authored papers are fine; they’re often necessary. Yet there’s something inertial or status-quo-prejudiced with a co-authored paper. Everyone does have to agree, right? In macro, single-authored papers may also be in decline, but they’re still relatively more common than in micro. And there’s something more revolution-friendly about that. Einstein didn’t co-author the general theory of relativity.

One of my concerns about economics is we’re too consensus-oriented at the refereeing stage, at the editing stage, and even at the co-authoring stage. Again, I don’t know how to say co-authoring doesn’t make sense. Papers are harder to do than before, and you need all these different skills. But I think it’s a problem we should talk about more.

“We’re at a point where you can often believe the result of a paper.”

Several decades ago, a lot of econometrics papers were based on running correlations in various ways and of varying degrees of complexity. Then there’d be some part of the paper later on where you’d wave your hands and tell a story about causation or make some remarks about what you might do someday to address causation. But a lot of what was there was actually fairly lame. You didn’t really know what was causing what and things were taken on faith, or you would refer to your theoretical framework. You’d think things like, well, I’m a monetarist or I believe in rational expectations, so I’m going to superimpose this story on the data. A lot of the macro of the 1980s and even the 1990s was like that.

If you try to do that today in papers, maybe you can still publish them in a lesser journal, but they don’t become influential papers. You need to set things up in a way that you’re actually attempting to see which variable is causing which variable. You do difference-in-differences, for instance, and you see that minimum wage laws were imposed first on these counties before other counties, and you look at the differential effect that that had. It’s not quite proof of causality, but it’s way better than what we used to do. We’re at the point where you can often believe the result of the paper. That’s pretty good; not too long ago, we weren’t at that point. That, in a way, is a little scary.

Economic development typically involves a group of transitions, like the shift from agriculture to manufacturing to services. The Winter 2022 issue of the Journal of Economic Perspectives (where I work as Managing Editor) includes five papers on aspects of development-related transitions in the nations of Africa. Here are some of the big questions:

Does Africa have a manufacturing path to economic development?

In “Labor Productivity Growth and Industrialization in Africa,” Margaret McMillan and Albert Zeufack investigate Africa’s manufacturing sector. As they point out, a shift from agriculture to low-skilled manufacturing to high-skilled manufacturing to services has been a standard pattern of economic development for countries around the world. However, there are concerns that this path may not work well in the 21st century, because automated production keeps getting cheaper and thus reducing the opportunities for low-skilled jobs.

Some of the signs for industrialization in Africa are encouraging. The most comprehensive information about manufacturing employment in Africa only covers 18 countries, but based on those data, manufacturing employment in Africa’s lowand middle-income countries increased from 6 million to more than 20 million from 2000 to 2018, raising the share of employment in manufacturing from 7.2 percent to 8.4 percent (Kruse et al. 2021). In comparison, the 1990s saw zero growth in Africa’s manufacturing employment. Manufacturing exports from African nations have also grown at an annual average of 9.5 percent per year (Signé 2018). However, while employment and value-added shares of manufacturing in Africa are rising, both remain very low in comparison to the rest of the world …

But when the authors dig into the data, they find that the growth in manufacturing employment in nations of Africa has been primarily happening in small firms with less than 10 employees. Conversely, the growth in productivity in manufacturing in Africa is primarily in large firms, which aren’t adding many jobs. Many of Africa’s large manufacturing firms are in one way or another involves in processing of natural resources, which has been becoming an ever-more automation-intensive process.

Thus, the broad challenge for Africa’s manufacturing sector is for the larger firms to build linkages backward and forward into other African-based manufacturing firms, and for at least some of the small firms to make productivity gains and grow in size, so that they can become an “in-between” sector of manufacturing. One promising change is the African Continental Free Trade Area, started in 2018, which may offer possibilities for African-based manufacturing firms to sell and compete within a larger and more unified market. In addition, there are still some industries like certain kinds of textile manufacturing where low-wage labor can offer a comparative advantage in global production.

One common concern about manufacturing in Africa is also hard to wrap your hands around–the idea that there is a poor “business environment” in many nations. The authors point out that the relevant business environment comparison for many nations in Africa is countries like Bangladesh or Vietnam, and when you look at issues like transportation links or business conditions, a number of African nations do just fine in this comparison.

Much has been made of the poor business environment in Africa and business environment does matter, of course. But as nations across Asia have shown, where there are profits to be made, businesses find a way to work around business environment problems. Similarly, despite the business environment in Africa, formal manufacturing firms have performed well in terms of productivity growth (Diao et al. 2021). Indeed, measuring the business environment by the World Bank Doing Business index, many countries of Africa compare favorably to countries of Asia that have experienced rapid growth. In 2013, for example, Ghana ranked 27 countries ahead of Vietnam in the Doing Business indicators. … A comparison between the rankings of countries in Africa and those of countries in Asia with established bases in manufacturing for the year 2019 offers several similar examples. Rwanda ranks 40 points ahead of Vietnam at 29, Mauritius and Kenya are also ranked ahead of Vietnam at 21 and 61 respectively. Seventeen African countries rank ahead of Cambodia. Bangladesh has five million garment workers (ILO 2020), but out of 48 countries in Africa only eight countries are ranked below Bangladesh and seven of these countries are at war. Nigeria is ranked 30 points ahead of Bangladesh.

Can productivity growth in Africa’s agricultural sector push development forward?

The transition from agriculture to manufacturing involves both push and pull: increased productivity in agriculture freeing up workers to move to manufacturing, along with the pull of higher-paid manufacturing jobs. Tavneet Suri and Christopher Udry take on the topic of “Agricultural Technology in Africa.” As they describe it, agricultural technology in Africa is stagnating.

[A]griculture is almost 20 percent of GDP in Africa, compared with a world average of about 5 percent. Moreover, the share of agriculture in GDP of the African region has remained stable over the last 50 years, whereas the share for other regions that started high in 1970—South East Asia and South Asia—has fallen a lot. … [A]gricultural shares of employment have declined across regions of the world in the last 30 years. Africa now has the highest share of employment in agriculture at about 50 percent, given the declines in the South Asia region, while the world average of employment in agriculture is closer to 30 percent. … A first step towards structural transformation happens as the agricultural sector evolves from smallholder farmers growing mainly food crops (cereals) for self-consumption to larger scale farmers growing food crops primarily for sale. At present, about 80 percent of African farmers are smallholders with under two hectares of land, who together account for 40 percent of cultivated area …

Standard improvements in agricultural technology include types of irrigation, fertilizer, pesticides, mechanization, improved seeds, and access to markets. In their overview of the literature, there’s no single cause of these issues in Africa. The successful smaller-scale programs seem to involve a mix of training, credit, access to inputs, crop insurance, and market access. Scaling all of these up at once is a real task.

In addition, the authors emphasize that modern agricultural production is very responsive to specific conditions of the land and the terrain. It can make sense for neighboring farmers, or with a single farm, to use very different mixtures of crops and technology mixes. One role of agricultural R&D is to figure out how to get these ideal mixtures. The authors write that in India, “it is common to have 20–40 new varieties of rice released each year since 1970, along with 10–20 new varieties of both maize and wheat each year”–and the number of new varieties is rising over time. Similar patterns are not happening in much of African agriculture.

How will Africa’s women in workforce interact with economic change?

Women entering the (paid) workforce is a common signal of economic development: for example, it alters the incentives female education and for fertility. Taryn Dinkelman and L. Rachel Ngai discuss “Time Use and Gender in Africa in Times of Structural Transformation.” From the Appendix:

We highlight two stylized facts about women’s time use in Africa. First, in North Africa, women spend very few hours in market work and female labor force participation overall is extremely low. Second, although extensive margin participation of women is high in sub-Saharan Africa, women tend to work in the market for only a few hours each week, with the rest of their work hours spent in home production. These two facts suggest two different types of constraints that could slow down the reallocation of female time from home to market as economies grow: social norms related to women’s market work, and a lack of infrastructure (e.g., household infrastructure and childcare facilities) to facilitate marketizing home production.

The authors collect time use survey data to make a number of intriguing comparisons:

African housewives do not work significantly more hours per week in the home than do American housewives. In fact, in some countries, African housewives work fewer hours. In the United States in 2010, housewives spent on average 45.7 hours per week in home production: about the same amount of time spent by Moroccan (45.7 hours), Ghanaian (45.8 hours), and (2010) South African (45.7) housewives. Only Sierra Leonean and South African housewives in 2000 report more hours in home production than American housewives in 2010. …

For most African housewives, the bulk of their time is spent cooking, cleaning, and doing laundry. In South Africa, Ghana, and Morocco, cooking absorbs between one-third to just over one-half of all home production hours. Cleaning takes another 6–27 percent of home production time, while laundry takes 5–13 percent. In contrast, child- and elder-care take at most 21 percent of hours, and higher-skilled household management takes at most 15 percent of home production time. … The composition of home hours among modern US housewives is the exact reverse of South African, Ghanaian, and Moroccan housewives. Over half of home production hours in 2010 are spent in home management and in care work, with only 15 percent of hours spent cooking, 20 percent cleaning, and 8 percent doing the dreaded laundry. … Housewives in South Africa, Ghana, Morocco spend their time much more along the lines of American women in the 1920s and the 1960s.

Can the economies of Africa created the jobs needed for young adult workers?

With populations expanding in many African countries, a key question for economic and social stability is what jobs will be available for young adults. Oriana Bandiera, Ahmed Elsayed, Andrea Smurra and Céline Zipfel discuss this question in “Young Adults and Labor Markets in Africa.” They write: “Today, one of every five people who start looking for their first job is born in Africa. By 2050, it will be one in three …”

The authors emphasize that while labor force participation rates are similar in African nations to other countries at similar levels of development, the real gap is in the number of young adults with employers and steady salaries. They point out that in a comparison group of developing countries, it’s more common for the elderly–who entered the labor force at an earlier time in the development process–to be self-employed and not salaried, but in Africa countries, younger and older adults are about equally likely to be self-employed and not salaried. Thus, existing development in Africa is not leading to more young adults having salaried jobs.

What might be done about this? The authors discuss possibilities for vocational skills training on the labor supply side, and for policies like wage subsidies or providing credit to help firms expand their hiring on the labor demand side. I was especially intrigued by what the authors call “matching policies”–basically, in the context of some African nations, it can be hard for employees to pay application fees, and hard for employers to have confidence in who they are hiring. What seem like relatively small interventions, like having the government pay the application cost for workers, or having a job search agency that provides advice on job applications and interviews, together with some verifiable tests on skills and personality, can make a substantial difference.

Is the political economy of Africa primed for the changes of development?

For example, sub-Saharan Africa saw a dramatic rise in democratic institutions of governance during the third wave of democratization in the 1990s, with Zambia, Cape Verde, and Benin as salient examples. This was spurred by the spread of democratic ideas, the end of the Cold War and the fall of the Soviet Union, the creation of robust local democratic communities, and the implementation of economic reforms(Huntington 1991). While only Botswana and Mauritius held regular multipartyelections by 1989, 33 of the region’s countries had held at least two sets of elections by late 2003 (Crawford and Lynch 2012). Figure 1 illustrates this change with data from the widely used Polity V database, produced by the Center for Systemic Peace, which collects components of governing institutions in 167 countries. These components are merged into an overall scale ranging from –10 (think “hereditary monarchy”) to +10 (consolidated democracy). Autocracies are scored from –5 to –10, and as Figure 1 shows, sub-Saharan Africa as a whole was in that category for much of the 1970s and 1980s. Since then, the Polity score for sub-Saharan Africa has risen substantially, approaching average world levels.

Economic outcomes in sub-Saharan Africa have also been converging to world norms. During the past 20 years, average GDP per capita in sub-Saharan Africa has more than doubled: from about $600 to close to $1600 (comparison using current US dollars, World Development Indicators data, as of June 2021). This wave of economic growth across sub-Saharan Africa is admittedly uneven. But while some countries still lag, economic growth rates in Rwanda, Ghana, and Ethiopia over the past 20 years resemble those in China and India, and the regional growth rates for Africa are comparable to those in regions like East Asia and Latin America.

The authors argue that some of the most important reforms for nations in Africa may be to help political institutions function in the broader public interest. They discuss campaign contribution limits, especially from corporations that are involved with government contracts; creating a nonpartisan civil service; having certain industry regulators elected rather than appointed; audits of how local governments spend money; using biometric identification to assure that government payments actually reach the intended person; public town hall meetings and debates; and others.