I sometimes see articles that don’t feel worthy of a post here, but might interest the sort of discerning, intelligent, thoughtful, quirky, oddball readers who drop by this website. I tweet about these articles, but thought I might pass along some recent examples from the last week or so here as well. If you click on the image, it should take you to the underlying article.

From an Unapologetic Safety Regulator

Consumers may want more safety from the products they buy than unfettered market competition provides. Sure, market forces allow for certain firms to build up a reputation for safety (or lack of it) over time. Moreover, lawsuits can punish firms for unsafe products. But these forces operate imperfectly. After all, an “unsafe” product may be one that poses higher but not immediate risks, like when an electrical appliance is more likely to start a home fire and the stuffing in your future is more ignitable than you would have preferred. Also, the idea that reputation and lawsuits will provide an adequate level of safety operate by first letting a sufficient number of accidents happen so that a pattern is broadly recognized and publicized. It seems possible that a broad-scale effort in collecting information and looking patterns might at least in some cases accelerate the move to safer products

The Consumer Product Safety Commission came into existence in 1972, and by 1973, Robert S. Adler was a special assistant to one of the original commissioners. Adler’s career moved between academia (research and teaching on business law at the University of North Carolina) and government (among other stops, counsel to the Subcommittee on Health and the Environment of the Committee on Energy and Commerce in the U.S. House of Representatives). But he eventually came full circle back to the CPSC, where he was a commissioner from 2009-2021 (and acting chair the last two years). As practitioner, student, and teacher of business regulation, he has walked the walk. He offers some lessons about his experiences in “Reflections of an Unapologetic Safety Regulator” (Regulatory Review, October 17, 2022).

We’ve had the CPSC for 50 years now, and so we can observe some actual safety trends. Adler writes:

Similarly, in its almost 50 years of operation, the CPSC has seen substantial declines in death and injury in the face of a growing population: 43 percent reduction in residential fires, 80 percent reduction in crib deaths, 88 percent decline in baby walker injuries, 80 percent reduction in child poisonings, 35 percent decline in bicycle injury rates, 55 percent decline in injuries from in-ground swimming pools, and the virtual elimination of child suffocations in refrigerators and fatalities from garage doors.

It is of course theoretically possible that these sorts of declines would have happened just as quickly, or faster, without a CPSC–under pressure of reputation effects and lawsuits. This leads to what Adler calls the Great Safety Paradox:

Paradoxically, the more successful regulators are in protecting the public, the less anyone notices. This paradox occurs because well-crafted safety rules do not raise prices or interfere with products’ utility. In such cases, no one notices the improvement in safety. Most parents do not realize that the cribs they place their infants in no longer permit them to slip between the slats and strangle. Nor do they understand how much safer and less lead-laden their children’s toys are. Similarly, most consumers will never recognize that their children no longer face being crushed by a garage door that unexpectedly closes on them or that infants do not suffocate in refrigerators because the doors can now be easily opened from within. Numerous government safety rules operate in a similar fashion, with life-saving benefits but little public recognition.

What about the costs of such regulations? As Adler emphasizes, the costs of a rule that makes the slats of infant cribs closer together is pretty minimal. The costs of people being injured by unsafe products are quite real. Adler:

When health and safety agencies write a safety rule, they do so to eliminate or reduce deaths and injuries that consumers suffer in product-related accidents. The CPSC estimates that roughly 31,000 people die and 34 million people suffer product-related injuries every year. These deaths and injuries impose significant costs on the economy—roughly one trillion dollars annually. They do so first as medical costs and lost wages, then as higher premiums for health insurance—or higher taxes to pay for the uninsured. Moreover, product-related tragedies almost always result in a loss of economic productivity of the victims, not to mention the pain and suffering they experience. Accordingly, the argument that regulations necessarily impose new costs on society is not persuasive. The costs in the form of deaths and injuries are already there, and often they impose as much of a drag on the economy as any safety rule.

What about alternative, like, recalls of unsafe products? This can work to some extent, but a common patterns is that a relatively small share of products are returned to the manufacturer–and this typically only happens after the CPSC is involves. What about education about safe use? This can sometime be effective, over time, as in the case of government anti-smoking announcements and warning requirements. But public safety campaigns often cost a lot, for at best modest responses:

As former CPSC Commissioner R. David Pittle once said, “it is far easier to redesign products than it is to redesign consumers.” Regulators have undertaken education campaigns intending to produce substantial changes in consumer behavior with limited success. …

In the early 1980s, for example, NHTSA undertook a massive multiyear national campaign to encourage consumers to wear seatbelts. After spending millions of dollars on the campaign, the agency revealed that the rate of seatbelt use rose only from about 11 percent to 14 percent—a disappointing result however one looks at it. The seatbelt usage rate did not significantly increase until the U.S. Department of Transportation pressured the states to enact mandatory seatbelt laws.

What about industry getting together to set standards? For example, the companies that make portable generators recently got together to set voluntary standards for mitigating the risk of carbon monoxide poisoning. The CPSC had no big quarrel with the standards themselves–except that the same companies that had promulgated the standards were not actually living up to them, and 500 or so people each year are dying as a result. Industry participation in making safer products can be truly useful, but without a government agency, industry compliance with voluntary standards may not be high.

Adler is clearly a regulation fan-boy (not that there’s anything wrong with that!), and he probably has a tendency to overstate benefits and understate costs. It’s also worth noting that requiring safer design of consumer products is a particular regulatory task, with different types of tradeoffs than other prominent regulators like the Environmental Protection Agency or the Food and Drug Administration. I know regulators can overreach on safety issues, or become focused on overly costly approaches. But markets can also underreach on consumer safety issues. The real-world answer would seem to involve pushing-and-pulling between the two, with the arguments conducted quantitatively and out in the open.

The White-Black Wealth Ratio Since 1870

Wealth represents the accumulation of assets during a lifetime, and thus wealth gap are always larger than income gaps. Nonetheless, the wealth gaps between black and white Americans are remarkable. Ellora Derenoncourt, Chi Hyun Kim. Moritz Kuhn, and Moritz Schularick have done a deep dive into historical record to develop some estimates in ” Wealth of Two Nations: The U.S. Racial Wealth Gap, 1860-2020″ (Federal Reserve Bank of Minneapolis, Opportunity & Inclusive Growth Institute Working Paper 59, June 10, 2022). There’s also a readable overview of the main findings by Lisa Camner McKay, “How the racial wealth gap has evolved—and why it persists: New dataset identifies the causes of today’s wealth gap” (October 3, 2022).

Here’s a summary figure. The vertical axis measures average per capita white/black wealth as a multiple: that is, back in 1860, the average white person had more than 50 times the wealth of the average black person on a per capita basis, but now the multiple is more like six time.

Clearly, the drop in the white-to-black wealth ratio was fastest back in the 19th century. About one-quarter of the convergence can be explained by the white slaveholders’ loss of slaves as part of their “wealth,” but the rest of the convergence happened as wealth of blacks grew relatively more rapidly than that of whites.

Then the white-to-black ratio levels out from 1900 up to about 1930, during a time of legalized discrimination and segregation for black Americans. There is some move toward greater equality of wealth after World War II, and an additional move after the passage of the Civil Rights Act of 1964. But there has been a move toward greater inequality since about 1980, which seems mainly due to the fact that those who already had the resources to own housing or to have stock market investments have done especially well since then, while those who did not already own such assets had no way to benefit from the capital gains that have occurred.

As Camner McKay summarizes the work:

The role of capital gains is particularly important here. The high rate of return to capital holdings over the last 40 years—economic parlance for “stocks have really gone up a lot”—is a leading cause of the wealth dispersion in the United States today. According to analysis by economist Emmanuel Saez and others, wealth has become significantly more concentrated during this period: In 1980, the richest 0.1 percent of Americans—about 160,000 households—owned 7.7 percent of national wealth. In 2020, they owned 18.5 percent. “Given that there are so few Black households at the top of the wealth distribution,” Derenoncourt and co-authors write, “faster growth in wealth at the top will lead to further increases in racial wealth inequality.”

Here’s another way to slice the data, comparing the black share of the US population to the black share of total wealth.

One can of course raise a bunch of questions about the details, which in turn are addressed in the working paper. For example, where is the data from?

We do this by digitizing 50 years of data on Black wealth, from the 1860s to the 1910s, from southern state tax reports and combining this with information from the complete-count digitized censuses of 1860 and 1870. We extend this time series through the mid-20th century using historical estimates of total Black and national wealth, verified using the census of agriculture and population and household survey data from the 1930s. Finally, we draw on newly compiled data from historical and modern waves of the Survey of Consumer Finances to complete our coverage from 1949 to 2019 …

And yes, the data is publicly available at https://www.elloraderenoncourt.com/us-inequality-data.

There’s a lot that can be said about all this, but I’ll limit myself to the obvious: Four decades–call it two generations–of no progress on the white-to-black wealth ratio is a long, long time.

Africa: Too Many Currencies?

It is commonplace to observe that the enormous US domestic market benefits from having a single currency, rather than, say, 50 state-level currencies. Indeed, the case for a single currency across a broad market was compelling enough to persuade 19 of the 27 countries in the European Union to trade in their historically separate currencies for the euro. In contrast, the nations of Africa have 42 separate currencies.

There is a newly-founded African Continental Free Trade Area, seeking to reduce barriers to trade and investment across the countries of within Africa. It could offer a real boost to productivity and growth across Africa: a June 2022 World Bank study estimates that it could “bring income gains of 9 percent by 2035 and reduce extreme poverty by 50 million.” But for trade to work, it has to overcome the problems of 42 currencies. Chris Wellisz provides an overview in “Freeing Foreign Exchange in Africa” (Finance & Development, September 2022). He writes:

Making payments from one African country to another isn’t easy. Just ask Nana Yaw Owusu Banahene, who lives in Ghana and recently paid a lawyer in nearby Nigeria for his services. “It took two weeks for the guy to receive the money,” Owusu Banahene says. The cost of the $100 transaction? Almost $40. “Using the banking system is a very difficult process,” he says.

His experience is a small example of a much bigger problem for Africa’s economic development—the expense and difficulty of making payments across borders. It is one reason trade among Africa’s 55 countries amounts to only about 15 percent of their total imports and exports. By contrast, an estimated 60 percent of Asian trade takes place within the continent. In the European Union, the proportion is roughly 70 percent.

What are the options here? In theory, it would be possible for countries across Africa to unite with a single currency of their own. In practice, this seems pretty unlikely. At present, there are 14 countries in Africa that use the “CFA franc” as their currency: six in central Africa (Cameroon, the Central African Republic, Chad, the Congo, Equatorial Guinea and Gabon) and eight in west Africa (Benin, Burkina Faso, Côte d’Ivoire, Guinea Bissau, Mali, Niger, Senegal and Togo). Indeed, there are technically two different CFA francs, one for each of these regions, but their exchange rate in terms of euros is always the same. Together, these countries comprise about one-eighth of Africa’s GDP.

Current perceptions of the CFA franc are, at best, only partially favorable. It has provided monetary stability, but at times the exchange rate value of the currency has been so high that it strangled exports from these countries. It’s also a legacy of colonialism by France. The current plan seems to be that the west African version of the CFA franc will be phased out in favor of a shared currency called the “eco,” which may be more widely used across other nations of west Africa. But the potential transition is scheduled for a few years away, and it’s unclear (at least to me), whether the countries using the central African version of the CFA franc will join in. There’s a lot of talk about “taking back control of the currency,” but the current proposals for the “eco” would continue to have a fixed exchange rate with the euro.

In short, the existing currency unions in Africa are being sharply question and seem to be in transition. A even broader currency union isn’t on the table. And frankly, it’s not obvious that a broader currency for Africa is a good idea at this moment in time. A shared currency across a geographic area works best when the economy of that area is already somewhat united by flows of goods and services, finances and people, and shared government programs. Obviously, the question of whether, say, Greece should share a currency with Germany, has posed real problems for the euro.

So the current plan, as Wellicz describes it, is to create a Pan African Payment and Settlement System (PAPSS):

The system aims to link African central banks, commercial banks, and fintechs into a network that would enable quick and inexpensive transactions among any of the continent’s 42 currencies. … PAPSS aims to solve such problems by settling transactions in local African currencies, obviating the need to convert them into dollars or euros before swapping them for another African currency. In essence, PAPSS would eliminate costly overseas intermediaries. The system aims to complete transactions in less than two minutes at a low though unspecified cost.

The careful reader will note that this description makes heavy use of “aims to.” PAPSS was apparently formally launched in January 2022, but had not cleared any commercial transactions through this summer. The success of Africa’s efforts to promote trade across the continent may well depend on whether PAPSS or a similar arrangement can succeed.

For broader discussion of issues facing the economies of nations across Africa, a useful starting point is the five-paper symposium in the Winter 2022 issue of the Journal of Economic Perspectives (where I work a Managing Editor). As always, the articles are all freely available online:

- “Labor Productivity Growth and Industrialization in Africa,” by Margaret McMillan and Albert Zeufack

- “Agricultural Technology in Africa,” by Tavneet Suri and Christopher Udry

- “Time Use and Gender in Africa in Times of Structural Transformation,” by Taryn Dinkelman and L. Rachel Ngai

- “Young Adults and Labor Markets in Africa,” by Oriana Bandiera, Ahmed Elsayed, Andrea Smurra and Céline Zipfel

- “Political Distortions, State Capture, and Economic Development in Africa,”: by Nathan Canen and Leonard Wantchekon

Monetary Tightening: Previous US Episodes

As the Federal Reserve raises US interest rates in an effort to quell inflation, are there any lessons to be learned from similar previous episodes. The most recent Global Financial Stability Report from the IMF offers some discussion.

Here’s a figure showing the patterns of past monetary tightening back to 1960. The figure is a little busy, here’s what you’re looking at. The shaded areas are when recessions occurred, with the horizontal black lines near the bottom of the figure showing the total decline during each given recession. The yellow line is the rate of inflation. The red line shows the federal funds interest rate, which is the policy rate targeted by the Fed: this is shown as a solid red line during periods when the Fed is raising interest rates, but as a dashed red line at other times. The blue line shows the yields on 10-year US Treasury bonds which can be viewed as one way of measuring market interest rates.

What might we learn from these patterns? In some cases, the monetary tightening and higher interest rates was followed by no recession at all (1965, 1984, and 1994) or by rather small recessions (1970 and 2001). What are the chances that we sidestep a substantial recession this time? The IMF offers a mixed view. On one side:

In terms of inflation levels, the current period resembles more closely the 1970s and

early 1980s, when recessions following tightening cycles were characterized by high inflation and low growth (so-called stagflation). In those episodes, a substantial rise in the policy rate was necessary to tame inflation, followed by significant economic downturns.

On the other side;

While the current inflationary environment may be reminiscent of the 1970s or early 1980s, the nature of the COVID-19 shock is unprecedented. Moreover, the policy framework today is also very different. The Federal Reserve benefits from inflation-fighting

credibility built over the past several decades, helping long-term inflation expectations remain much better anchored. That said, financial vulnerabilities have emerged in some sectors in the wake of the COVID pandemic, and financial market volatility has notably risen after having remained relatively compressed over the preceding protracted period of low rates. The financial and regulatory architecture, however, has evolved considerably since the global financial crisis, and policymakers today have at their disposal a number of risk management tools that could be used to deal with the potential adverse systemic fallout from a disorderly tightening in financial conditions.

Finally, I’d just add that in past cycles of monetary tightening, the federal funds interest rate (red line) was consistently raised to a point where it was at or above the inflation rate (yellow line). In other words, the real interest rate (nominal interest rate minus inflation rate) was positive. However, in the current situation, the federal funds interest rate remains well below the inflation rate (red line below yellow line on the far right of the figure). The real federal funds interest rate has been negative most of the time since 2008. In addition, market interest rates as proxied by the 10-year Treasury bond yields has historically been (mostly) at or above the inflation rate, but even after recent increases, it remains well below the current inflation rate.

Thus, the policy question for the present is whether making the policy interest rate less negative, in a situation with negative market interest rates, will be enough to bring down inflation. A key element to this question is whether the inflation rate is being partly driven by temporary factors–price increases linked to the Russia-Ukraine war, as well as ongoing supply chain problems and other disruptions from the pandemic.

It seems to me that the Fed is (in effect) hoping that some of the existing inflation will fade on its own, and that its step-by-step increases in interest rates will be sufficient to knock out any remaining inflation. In this scenario, the current procession of monetary tightening might be followed by lower inflation with no recession or only a modest recession. On the other side, it’s possible for inflation to begin from one-time causes, but then develop its own ongoing momentum. If the existing inflation doesn’t fade on its own, then the Fed seems committed to an ongoing succession of higher and higher interest rates, and a significant recession sometime next year becomes more likely.

Ethanol Controversies, Redux

From the standpoint of producing carbon-free energy, using ethanol to supplement gasoline might seem like a no-brainer. Ethanol comes from crops like corn, which collect carbon from the atmosphere as they grow. When the ethanol is burned, it does releases carbon into the atmosphere–but then carbon can again be collected in the next corn crop. But of course, nothing is that simple. Corn needs to be grown, typically using machinery and fertilizer, and then processed into ethanol, all of which require energy inputs. If growing additional corn for ethanol requires cultivation of additional land, plowing and preparing that land will release substantial amounts of carbon dioxide. Moreover, the use of corn for ethanol drives up demand for corn and keeps the price of corn higher than it would otherwise be, which is a political selling point for US farmers, but can put stress on the diets of the poor–especially in developing economies.

These issues have bubbled up again with the disruption of agricultural markets due to Russia’s invasion of Ukraine, combined with the ongoing global supply chain disruptions, but the topic isn’t new. Back in 2011, I amused myself for a few months at this blog by posting examples about of international organizations that had come out against subsidizing biofuels like ethanol. For example, in a June 2011 post, ”Everyone Hates Biofuels,” I pointed out a report in which 10 international agencies made an unambiguous proposal that high-income countries drop their subsidies for biofuels. I followed up with ”The Committee on World Food Security Hates Biofuels” in August 2011 and ”More on Hating Biofuels: The National Research Council” in October 2011. For a couple of additional whacks at the pinata, see “Biofuels and Hunger in Low-Income Countries” in January 2013 and “Against Biofuel Subsidies” in June 2015.

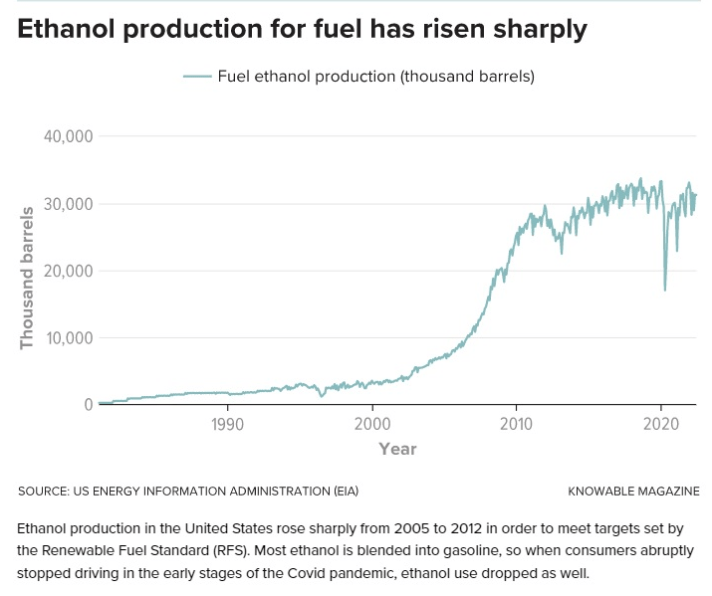

For an update, Dan Charles focuses on the environmental issues in a readable essay “How green are biofuels? Scientists are at loggerheads” (Knowable Magazine, October 6, 2022). Here’s a figure showing the rise in US ethanol production, which was launched to higher level starting in 2005 with a mixture of government requirements and subsidies.

Charles emphasizes some useful points about where the argument over biofuels currently stands. One key issue dividing supporters and opponents is the extent to which corn grown for ethanol affects land use. On one side, there is a detailed and comprehensive model of land use called the Global Trade Analysis Project at Purdue University, or GTAP-BIO, which broadly suggests that the rise of ethanol hasn’t cause much additional land to come under cultivation but instead has been enabled by higher crop productivity on existing land.

On the other side, the crops for ethanol have to come from somewhere. Charles writes:

Ethanol factories now consume about 130 million metric tons of corn every year. It’s about a third of the country’s total corn harvest, and growing that corn requires more than 100,000 square kilometers of land. In addition, more than 4 million metric tons of soybean oil is turned into diesel fuel annually, and that number is growing fast.

Charles notes that the amount of US farmland under cultivation had been gradually declining from the 1980s up until the passage of the Renewable Fuel Standard in 2007. At this point, the decline in cropland stopped–because of the rise in corn and soybean production for biofuels. “Without the ethanol boom, the pre-2007 trend in land use would have continued. More land — 5 million acres — would have remained in grass between 2008 and 2016, rather than being converted to grow crops.” Thus, it can simultaneously be true that crops for ethanol have not dramatically expanded land under cultivation, and also that without crops for ethanol, there would be substantially less land under cultivation.

If we work from the political assumption that US corn and soybean farmers are a potent and focused special interest, and that their Congressional representatives will be able to block the withdrawal of ethanol requirements and subsidies for the indefinite future, what are the possible next steps here? There seem to be two answers on which supporters and opponents of ethanol can more-or-less agree.

One approach “is figuring out ways to measure those environmental benefits and pay landowners for them, just as they get paid for growing corn. To some extent, the US Department of Agriculture does this already, with programs that pay farmers to preserve areas of grassland or forest. Such initiatives are set to expand; the Inflation Reduction Act, which Congress passed in August, gives them an extra $18 billion in funding.”

The other approach is technological. For some years now, there has been discussion of “cellulosic biomass,” which involves getting ethanol from prairie grasses. This transmutation is possible in a laboratory, at high cost, but it seems far from being a commercial proposition. But if the process was commercially viable: “The grass could be harvested, leaving the roots to grow undisturbed, building up carbon-rich organic matter in the soil and avoiding most of the environmental damage that results from converting land into cornfields.”

Ultimately, the idea of using corn and soybeans as a primary energy source doesn’t seem like sensible policy, whether the goals are environmental or to ensure affordable global food supplies. Charles writes:

[T]he world’s croplands, which have claimed vast ecosystems, cover less than half an acre per person on the planet. Producing enough biofuel to power one typical passenger car, meanwhile, requires more than 1.2 acres. (Photovoltaic solar arrays produce many times more usable energy per acre of land than biofuels, and can also be located in dry areas that can’t grow food.)

A Nobel for Insights About Banks and Financial Crises: Bernanke, Diamond, and Dybvig

As time goes by, I find it increasingly hard to explain to the non-econ world just what happened back in September 2008, when during a period of perhaps 2-3 weeks there seemed to me a meaningful chance (and by “meaningful,” I mean large enough to keep me awake at night) that the US banking and financial sector would melt down in a way that would have led not just to the substantial recession that did occur, but to something much worse. But in one of those odd quirks of history, the Federal Reserve at that time was being chaired by a former academic economist named Ben Bernanke who was actually a recognized expert in the subject of banking and financial collapses, based on research that he and others like Douglas Diamond and Philip Dybvig had done back in the 1980s and 1990s. The Great Recession from 2007-2009 was very bad, and it could have been so much worse.

The Royal Swedish Academy of Sciences has now awarded what is formally known as the “Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2022” to Bernanke, Diamond, and Dybvig “for research on banks and financial crises.” As usual, the prize committee has published two explanatory pieces for those who want to know what the fuss is all about. There’s a shorter “popular science background” article called “The laureates explained the central role of banks in financial crises,” and a longer and more technical (that is, about 70 pages) “scientific background article titled “Financial Intermediation and the Economy.” Earlier narratives tended to describe the “Great” character of the Depression as a list of poor decisions and things that went wrong. Bernanke made a strong case that the length and depth of the Great Depression was intimately tied to one main cause: the crisis fo the banking system at the time. The prize committee writes:

Prior to Bernanke’s study, the general perception was that the banking crisis was a consequence of a declining economy, rather than a cause of it. Instead, Bernanke established that bank collapses were decisive for the recession developing into deep and prolonged depression. Once a bank goes bankrupt, the relationship between the bank and its borrowers is cut; this relationship contains knowledge capital that is necessary for the bank to manage its lending efficiently. The bank knows its borrowers, it has detailed information about what borrowers have used the money for and what requirements are needed to ensure the loan will be repaid. Building up such knowledge capital takes

a long while, and it cannot simply be transferred to other lenders when a bank fails. Repairing a failed banking system can therefore take many years, during which time the economy functions very poorly. Bernanke demonstrated that the economy did not start to recover until the state finally implemented powerful measures to prevent additional bank panics.

At about the same time in the early 1980s, Diamond and Dybvig were developing a theoretical model of banking and the financial sector that addressed these issues. They began with the basic idea of a bank as a “financial intermediary”–that is, some economic agents (people and firms) have savings they would prefer not to spend in the present, while others would like to borrow and spend now, and then repay later. Banks serve as the intermediaries between these groups.

But an immediate challenge arises here. What is a substantial number of savers been decide to withdraw their money from these theoretical banks, perhaps because the savers don’t trust that their savings are safe at the bank? The theoretical bank will not have the money for everyone: after all, that money has already been loaned out to people who borrowed to purchase homes and cars, and to businesses who borrowed to make investments. Thus, there is a possibility of a “bank run,” where people rush to the theoretical bank and try to withdraw their funds right now–and in doing so, they make it impossible for the bank to continue functioning.

The bank run is of course a staple of stories and accounts of the time before the 1930s: two of the best-known examples from movies are from Jimmy Stewart in It’s a Wonderful Life and when the little boy Michael tries to withdraw his tuppence from the bank run by Dick van Dyke in Mary Poppins. However, if the government provides deposit insurance, then there is no reason for bank runs. From this perspective, it isn’t a coincidence that when federal bank deposit insurance was enacted in 1933, he role of the fragile banking system in propagating the Depression faded away, and the worst of the Great Depression ended.

But a follow-up tradeoff emerges here. If there is bank deposit insurance, then savers no longer need to worry about whether the bank is making sensible decisions about lending, or whether the bankers are chasing higher risks and perhaps higher payoffs. Thus, Diamond in particular emphasized that deposit insurance needs to be paired with government oversight of banks to make sure that they are not taking undue risks. This pairing of deposit insurance and financial oversight of banks functioned to keep the US banking and financial system stable for a number of decades.

But there were warning signs that not all the problems has been addressed. Perhaps most notably, during the savings and loan crisis of the later 1980s, a number of S&Ls found themselves in a bad financial situation: they had made long-term loans for home mortgages over the previous decades at relatively low interest rates, but the high rates of inflation in the 1970s had pushed up interest rates. Under law, the S&Ls were limited in the interest rates they could pay, so savers instead wanted to move their funds to money market accounts, which didn’t have the same restrictions. This was a modern kind of bank run: funds being withdrawn from one part of the financial sector and moved to another. A number of the S&Ls were faced with bankruptcy as their deposits diminished, and some of the managers chose the strategy of making risky loans at high interest rates to try to regain solvency. Some politicians pressured the financial regulators of their local financial institutions not to crack down. Ultimately, federal government ended up needing to pay off more than $150 billion to protect depositors who had kept funds in these institutions. For more background, readers could start with the three-paper symposium in the Fall 1989 issue of Journal of Economic Perspectives.

With the Great Recession of 2007-9, a somewhat similar problem arose again. A substantial and growing part of the US financial sector had moved outside banks, into what is often called the “shadow banking” sector. If you wanted a loan for a house, you could get it through a non-bank institution, and behind the scenes, mortgage loans were repackaged and sold to investors like pension funds or insurance companies. Businesses found other ways to borrow as well, by using bond markets as well as their own versions of loans that were repackaged and resold. These shadow banking financial institutions were not under the rules of federal deposit insurance or the prudential scrutiny of federal bank regulators. Risky loans were made. And when the shadow banking institutions went sideways, the actual banking system was threatened as well. It was extraordinarily important to have a knowledge base, and people in charge who understood that knowledge base, to recognize that the dire problems of financial institutions in 2007 and 2008 should not just be viewed as an outcome of mortgage sector problems, but that these issues could become a cause of additional and deeper problems.

These underlying problems persist today. Every new innovation in the broader financial sector–the shadow-banking sector–raises the issue of possible financial runs from one sector to another, along with questions of how government might create (or not!) some combination of safety guarantees and a regulatory apparatus. The Nobel prize committee wrote:

Banks and bank-like institutions have existed for thousands of years. Today they are active in every country around the world. Banks obviously perform important functions, but they have also been at the epicenter of some of history’s most devastating economic crises such as the Great Depression. Nevertheless, it was not until the work of this year’s laureates, Ben S. Bernanke, Douglas W. Diamond, and Philip H. Dybvig, that we had a comprehensive theory of why banks exist in the form we observe, what role they play in the economy, why they are fragile, and an empirical account of how devastating

and long-lasting the consequences of massive bank failures can be. …The research from the 1980s for which this year’s Prize in Economic Sciences is awarded obviously does not provide us with final policy recommendations. Deposit insurance does not always work as intended. It can lead to perverse incentives for banks and their owners to gamble to take the profit if things go well and let taxpayers pay the bill if not. Runs on new financial intermediaries, engaging in profitable maturity transformation like banks, but operating outside of bank regulation, were arguably key for the financial crisis 2007–2009 leading to the Great Recession. When central banks act as lenders of last resort, this can lead to large and unintended wealth redistribution and have negative moral hazard

effects on banks who may increase reckless lending, potentially leading to future crises.How to regulate the financial market so that it can perform its important function of channeling savings to productive investments, without from time to time causing financial crises, is a question that is actively debated to this day. The same is true about what policies are most effective in preventing a threatening crisis from developing. However, based on the foundational work of the laureates and all research that has followed, society is now better equipped to handle financial crises.

Why Do So Many Interventions Help Women, but Not Men?

Richard V. Reeves points out a disconcerting finding: in studies of interventions that seek to boost the life prospects of the disadvantaged, when positive effects are found, the benefits tend to accrue to women, not men. He discusses the findings in “Why Men Are Hard to Help,” appearing in the most recent issue of National Affairs. The essay is adapted from his recent book: Of Boys and Men: Why the Modern Male Is Struggling, Why It Matters, and What to Do about It. Some examples:

Thanks to a group of anonymous benefactors, students educated in the city’s K-12 school system receive paid tuition at almost any college in the state. Other cities have similar initiatives, but the Kalamazoo Promise is unusually generous. It’s also one of the few programs of its kind to have been robustly evaluated — in this case by Timothy Bartik, Brad Hershbein, and Marta Lachowska of the Upjohn Institute. They found that the Kalamazoo Promise made a major difference in the lives of its beneficiaries — more so than other, similar programs made in theirs. But the average impact disguises a stark gender divide. According to the evaluation team, women in the program “experience very large gains,” including an increase of 45% in college-completion rates, while “men seem to experience zero benefit.” The cost-benefit analysis showed an overall gain of $69,000 per female participant — a return on investment of at least 12% — compared to an overall loss of $21,000 for each male participant. In short, for men, the program was both costly and ineffective.

One of the other studies that jumped off my desk in considering this evidence was an evaluation of a mentoring and support program called “Stay the Course” at Tarrant County College, a two-year community college in Fort Worth, Texas. Community colleges are a cornerstone of the American education system, serving around 7.7 million students — largely from middle- and lower-class families. But there is a completion crisis in the sector: Only about half the students who enroll end up with a qualification (or transfer to a four-year college) within three years of enrolling. Many of these schools produce more dropouts than diplomas. The good news is that there are programs, like Stay the Course, that can boost the chances of a student succeeding. The bad news is that, as the Fort Worth pilot shows, they might not work for men, who are most at risk of dropping out in the first place. Among women, the Fort Worth initiative tripled associate-degree completion. This is a huge finding: That kind of effect is rare in any social-policy intervention. But as with free college in Kalamazoo, the program had no impact on college completion rates for men.

But Stay the Course and the Kalamazoo Promise are just two among dozens of initiatives in education that seem not to benefit boys or men. An evaluation of three preschool programs — Abecedarian, Perry, and the early Training Project — for example, showed “substantial” long-term benefits for girls but “no significant long-term benefits for boys.” Project READS, a North Carolina summer reading program, boosted literacy scores “significantly” for third-grade girls — giving them the equivalent of a six-week acceleration in learning — but there was a “negative and insignificant reading score effect” for boys. …

Students who attended their first-choice high school in Charlotte, North Carolina, after taking part in a school-choice lottery earned higher GPAs, took more Advanced Placement classes, and were more likely to go on to enroll in college than their peers — but the overall gains were “driven entirely by girls.” A new mentoring program for high-school seniors in New Hampshire almost doubled the number of girls enrolling in a four-year college, but it had “no average effect” for boys. Urban boarding schools in Baltimore and Washington, D.C., boosted academic performance among low-income black students, but only female ones. College scholarship programs in Arkansas and Georgia increased the number of women earning a degree but had “muted” effects on white men and “mixed and noisy” results for black and Hispanic men.

And so on, and so on, for studies of the effects of wage subsidies, worker training, and other areas. Reeves notes that a number of studies of such programs point out the gap between outcomes for boys and girls, or men and women, and then note (as academic research papers love to do) that it deserves further study. But those further studies–much less proposals for policies that would have improved outcomes for men–don’t seem to happen.

Thus, Reeves, like the rest of us, ends up falling back on explanations that have a plausible ring, but aren’t exactly the result of gold standard cause-and-effect social science research. He writes: “The problem is not that men have fewer opportunities; it’s that they are not seizing them. The challenge seems to be a general decline in agency, ambition, and motivation.” I

Reeves also notes: “[W]here there is a difference by gender, it is essentially always in favor of girls and women. The only real exception to this rule is in some vocational programs or institutions, which do seem to benefit men more than women — one among many reasons we need more of them.” Perhaps such programs speak more clearly to those with lower agency, ambition, and motivation?

If women had dramatically lower rates of college attendance, it would be viewed as a national problem. Indeed, it was viewed that way. As Reeves notes:

In 1972, Congress passed Title IX — a landmark statute to promote gender equality in higher education. Quite rightly, too: At the time, there was a 13 percentage-point gap in the proportion of bachelor’s degrees going to men compared to women. Just a decade later, the gap had closed. By 2019, the gender gap in bachelor’s degrees was 15 points — wider than it had been in 1972, but in the opposite direction. Today, women far outperform men in the American education system. … In the United States, for example, the 2020 drop in college enrollment was seven times greater for male students than for female students. At the same time, male students struggled more than female students with online learning.

Societies with a substantial proportion of disgruntled and flailing young men will suffer from an array of other related problems.

How Much of the Gasoline Price is Crude Oil?

The US Energy Information Administration gives this answer for August 2022:

I was buying gas recently, and because I was also picking up snacks, I went into the gas station to pay the cashier rather than swiping my credit card at the pump. I said something low-key conversational about “price of gas sure is up” and he visibly winced. So I added something like: “Of course, the gas station makes, what, about 5 cents when you sell a gallon of gas?” He visibly relaxed and even gave me a rueful smile. It made me suspect that the customer service people behind the counter, everywhere, have probably been taking a lot of face-to-face direct heat for higher prices.

Some Economics of Diapers

I remember family holidays when our children were little, where the first step was to grab a large suitcase and start packing in the diapers. But for a number of low-income US families, affording the diapers is a challenge to their limited resources. Jennifer Randles discusses “Fixing a Leaky U.S. Social Safety Net: Diapers, Policy, and Low-Income Families” (RSF: The Russell Sage Foundation Journal of the Social Sciences, August 2022, 8:5, 166-183). She writes (citations omitted):

Diaper need—lacking enough diapers to keep an infant dry, comfortable, and healthy—affects one in three mothers in the United States, where almost half of infants and toddlers live in low-income families. Diaper need … exacerbates food insecurity, can cause parents to miss work or school, and is predictive of maternal depression and anxiety. When associated with infrequent diaper changes, it can lead to diaper dermatitis (rash) and urinary tract and skin infections.

Infants in the United States will typically use more than six thousand diapers, costing at

least $1,500, before they are toilet trained . Cloth diapers are not a viable alternative for most low-income parents given high start-up and cleaning costs and childcare requirements for disposables. Many low-income parents must therefore devise

coping strategies, such as asking family or friends for diapers or diaper money; leaving

children in used diapers for longer; and diapering children in clothes and towels.Low-income parents also turn to diaper banks, which collect donations and purchase

bulk inventory for distribution to those in need and usually provide a supplemental supply of twenty to fifty diapers per child per month. In 2016, the nation’s more than three hundred diaper banks distributed fifty-two million diapers to more than 277,000 children, meeting only 4 percent of the estimated need. Many of those who seek diaper assistance

live in households with employed adults who have missed work because of diaper need. …

As a highly visible and costly item that must be procured frequently according to norms of proper parenting, diapers are part of negotiations about paternal responsibility

and access to children. Unemployed nonresidential fathers give more in-kind

support, such as diapers, than formal child support; the provision of diapers can be a form of or precursor to greater father involvement, especially among fathers who are disconnected from the labor market and adopt nonfinancial ideas of provisioning.

As Randles points out, some existing aid programs for poor families, like the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC) or food stamps, explicitly don’t cover diapers. She writes: “/The $75 average monthly diaper bill for one infant would alone account for 8 to 40 percent of the average state TANF [Temporary Assistance to Needy Families] benefit.” In addition, “[s]ince the onset of the COVID-19 pandemic, disposable diaper costs have increased 10 percent due to higher demand and input material costs, supply-chain disruptions, and shipping cost surges.”

Diapers are taken for granted as parents’ responsibility, but politically deemed a discretionary expense. This is misaligned with how mothers understood their infants’

specific basic needs, which for most came down to milk and diapers. Food stamps and

WIC offered support for one. No comparable acknowledgment or assistance for the other

meant that mothers struggled even more to access a necessity policy did not officially recognize their children have.

Several bills have been introduced in Congress in the last few years to provide diaper-focused assistance, but apparently none has made it out of committee. There are a number of state-level programs as well. Some are linked to what level of sales tax is imposed on diapers. Some seek to build up the supply at diaper banks. As another example, California gives voucher for diapers to TANF recipients who have children under the age of three.